CEST

21:57

TODAY’S WEATHER

Find information quickly and easily

Corporate

Income Tax Act 2010 Guidance Notes

- Guidance Notes for Companies

- Guidance Note CT100: How to complete Form CT1 - Corporate Tax Return

- Guidance Note CT101: How to complete Form CT3A - Authorising pour agents

- Classes of Expenditure allowed as Deductions

- Payments on Account Table - Schedule 10

- Guidance for split year treatment

Returns For Accounting Periods Ending On Or After 1st January 2011

- Form CT1 2018 (post 30-06-2024)

- Form CT1 2018 (01-07-2022 to 30-06-2024)

- Form CT1 2018 (pre 01-07-2022)

- CT2 - Return of Dividends

- CT2A - Additional Sheets

- CT2B - Additional Sheets

- CT2C - Additional Sheets

Corporate

- View Standard Industry Codes

- CT3 - Company Registration Spreadsheet

- CT3 - Company Registration Form

- 'CT3A - Authorising your Agent

- CT4 - Claim to reduce payments on account for an accounting period

- 'Country by Country Reporting - Notification Template

- 'Explanatory Notes on Country by Country Reporting Obligations

- Form ORC/1 - Application for Ordinarily Resident Certificate for a company

- Form CCC-1 - Request for Certificate of Compliance

Questions & Answers

Q. What is the standard rate of Corporation Tax?

A. The Corporation Tax rate for most companies in Gibraltar increased from 10% to 12.5% with effect from 1st August 2021 and then again to 15% with effect from 1st July 2024. Utility companies or companies enjoying a dominant market position continue to be liable at a higher rate of 20%. Included in the latter are companies providing electricity, fuel, water and telephony services.

Q. When does a company need to register with the Income Tax Office?

A. With effect from 1 January 2016, a company which is registered in Gibraltar under the Companies Act 2014, or has assessable income in Gibraltar under the Income Tax Act 2010, is required to register in Gibraltar for tax purposes.

Q. How does a company register with the Income Tax Office?

A. Companies should register with Companies House Gibraltar and will then be automatically registered for Corporate Tax purposes.

Q. When does a company have to submit a Tax Return?

A. A company shall submit a full and complete Tax Return within nine months after the end of the month in which the accounting period ends.

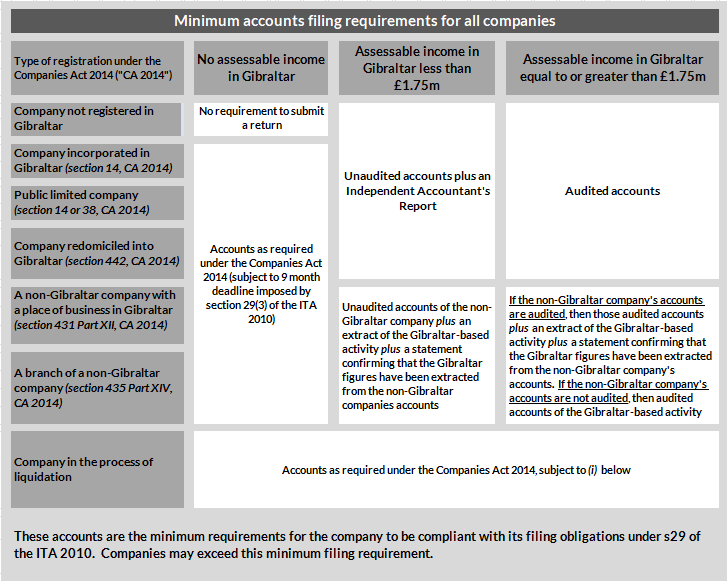

Q. What is a Complete Tax Return?

A. This is made up of the following documents:

- A completed and signed CT1 form

- Company accounts as per the tables below

- Tax computation if in receipt of any assessable income during the period

- PAYE reconciliation for any company that is not co-terminus with June and had any employees during the period

Q. What happens if a company misses a filing date?

A. If a complete Tax Return is not submitted within nine months after the end of the month in which the accounting period ends, penalties will be imposed accordingly. As from 1st January 2025 penalties will be issued as follows based on the company's size as determined by Schedule 9 of the Companies Act 2014 (see second table in the previous Q&A above):

|

|

Micro or Small |

Medium |

Large |

|

Due on the day immediately after the return is due |

£100 |

£750 |

£1,500 |

|

Due after 3 months from the return’s due date |

£450 |

£1,250 |

£3,500 |

|

Due after 6 months from the return’s due date |

£750 |

£2,000 |

£5,000 |

Prior to 1 January 2025, penalties were as follows for all companies:

- £50 on the day immediately after the return is due

- £300 after 3 months from the return’s due date

- £500 after 6 months from the return’s due date

You should note that legal action may be initiated at any point after initial default.

Q. What are 'Payments on Account' and when should these be paid?

A. These are advance payments of your company's tax liability, based on previous liabilities in accordance with the Payments on Account table in Schedule 10 of the Income Tax Act 2010. They are payable in two equal instalments by no later than the 28th February and 30th September, based on the company's financial period

Q. I have made both Payments on Account, do I need to make any further payment?

A. On submission of your complete Tax Return, you will be liable for a balancing tax payment if your taxable profits exceed the sum of the two Payments on Account paid for the same period. This additional liability will be payable within nine months after the end of the month in which the accounting period ends.

Q. What if I do not pay the full amount due?

If payments are not received on time, surcharges will be imposed. Please refer to table below.

|

SURCHARGES FOR LATE PAYMENT |

|

|---|---|

|

LENGTH OF DELAY |

SURCHARGE |

|

9 months after the company's financial period |

10% of outstanding corporate liability |

|

90 days after the 10% surcharge |

An additional 20% on the balance (i.e. tax plus surcharge) due. |

You should note that legal action may be initiated at any point after initial default.

A. If you are reasonably confident that your tax liability this year is going to be less than that of the previous year because your company has been less profitable this year, you are able to claim to reduce your Payments on Account via the CT4 form. This form will not be valid for any period which has already ended. Please note that surcharges will be incurred if, after having submitted such a claim, your accounts reflect that your actual tax liability exceeds the sum of the reduced payments on account already made.

Claim to Reduce Payments on Account - Form CT4

Q. My company has ceased to trade - what are my obligations?

A. The company should confirm its ceased trading date to the Income Tax Office in writing and continue filing complete returns up to the date it goes into liquidation or is struck off by Companies House. The company should also ensure that any outstanding liabilities with the Income Tax Office are paid.

For any enquiries please contact us on Tel. Nº 200 71071 or email us at